800+

Branches across all 4 provinces, AJK and GB

305 Schools

3 Colleges

Providing education to 47,000+ students

5.4 Million

Beneficiaries all over Pakistan

591,999+ Patients of Hepatitis and Diabetes treated free of cost

5.2 Million

Clothes collected & distributed amongst the needy

220 Billion

PKR Disbursed in interest-free micro-loans

2000+

Registered Khwajasiras receiving financial and social assistance

About us

About us

Since 2001, Akhuwat has been working for Poverty Alleviation

Akhuwat is a not-for-profit organization which was founded in 2001 on the Islamic principle of Mawakhat (مواخات) or solidarity. The concept of Mawakhat predates to 622 CE when Prophet Muhammad (Peace Be Upon Him) urged the residents of Medina (Ansars) to share half of their belongings with the Muhajirs (migrants) who were forced to flee persecution and migrated from Mecca to Medina.

Drawing inspiration from the generosity displayed by the Ansars, Akhuwat believes that if the same approach, where one affluent family embraces a less fortunate one is adopted today, inequality will be eradicated from the world. read more

Projects and Programs

Akhuwat

Islamic Microfinance

Rs.220

Billion Amount Disbursed

As Akhuwat’s core program, Akhuwat Islamic Microfinance (AIM) provides interest-free loans to the underprivileged to enable them in creating sustainable pathways out of poverty. With 800+ branches in over 400 cities across Pakistan, AIM is the largest interest-free microfinance program in the world, Alhamdulillah. Continue Reading

Akhuwat

Education Services

No society can prosper unless the fundamental right to education is granted to all of its citizens. Therefore, Akhuwat’s vision of creating a poverty-free society would remain incomplete unless the root cause; illiteracy, was addressed. Continue Reading

47,000+

Students

Akhuwat

Clothes Bank

3.0

Million Beneficiaries

3.23

Million Clothes Collected

Akhuwat Clothes Bank collects, sorts and cleans donated clothing & gifts and presents them to low-income families. These gifts are disbursed throughout the year while special campaigns are carried out during peak winter season and natural disasters. Continue Reading

Akhuwat Khwajasira

Support Program

The social and economic exclusion of the Khwajasira or transgender (Third Gender) community in Pakistan has left them dependent on alms, vulnerable to exploitation and increasingly susceptible to abuse. Realizing this and the consequent need for action in this arena, Akhuwat, in collaboration with Fountain House launched the Akhuwat Khwajasira Support Program in 2011. The program works with the vision of creating a system of support for members of the Khwajasira community. Continue Reading

2000+

Registered Khwajasira

Akhuwat

Health Services

591,999

Beneficiaries

Akhuwat Health Services (AHS) serves the poor through affordable and effective health care services. It provides subsidized medicines, lab tests, free examination and consultation to those families that are unable to afford basic health care. In 2009, AHS set up a health center in Township, Lahore… Continue Reading

News & updates

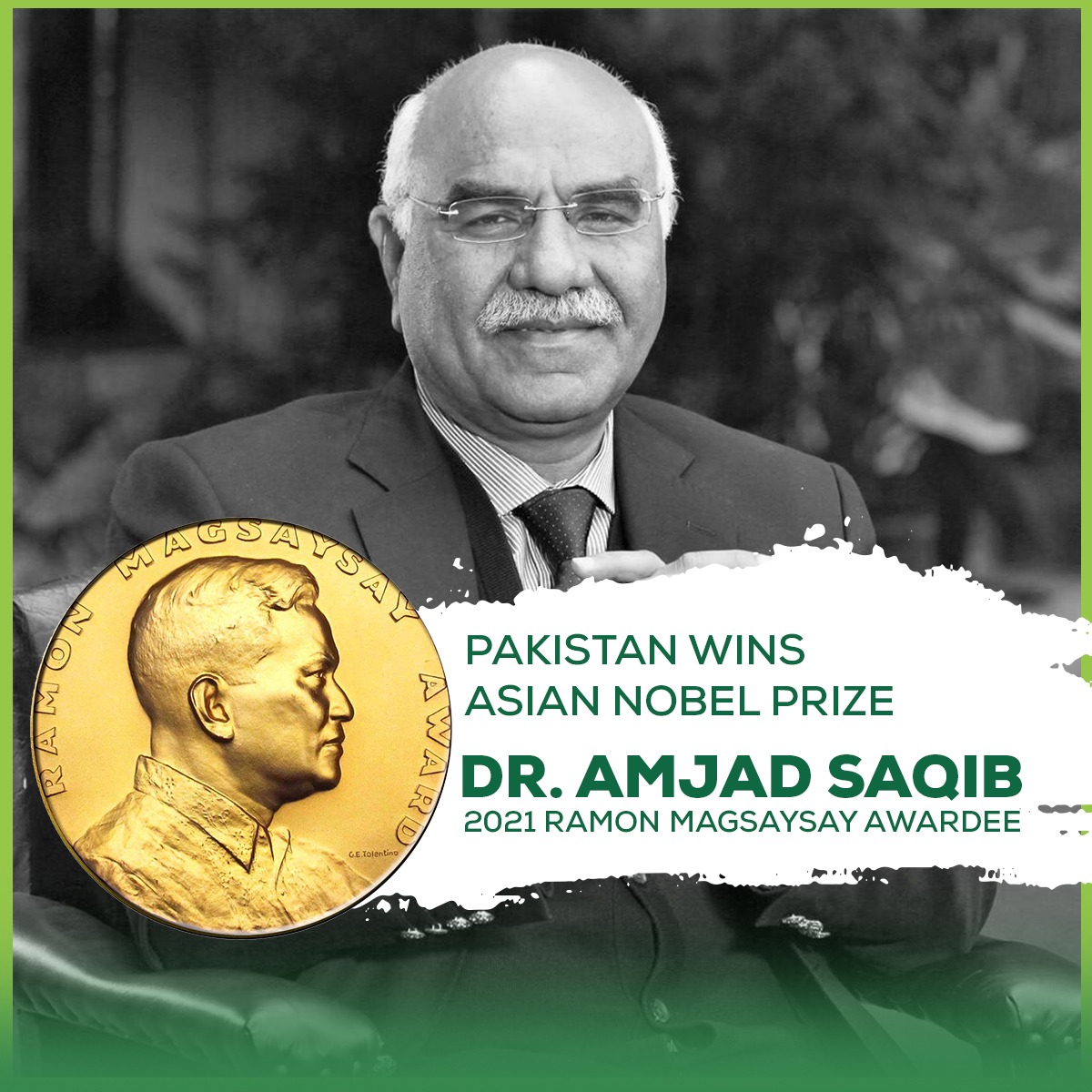

Ramon Magsaysay Award

Pakistan gets Ramon Magsaysay Award,

The Akhuwat Fellowship Program

The Akhuwat Fellowship Program seeks

Our Partners

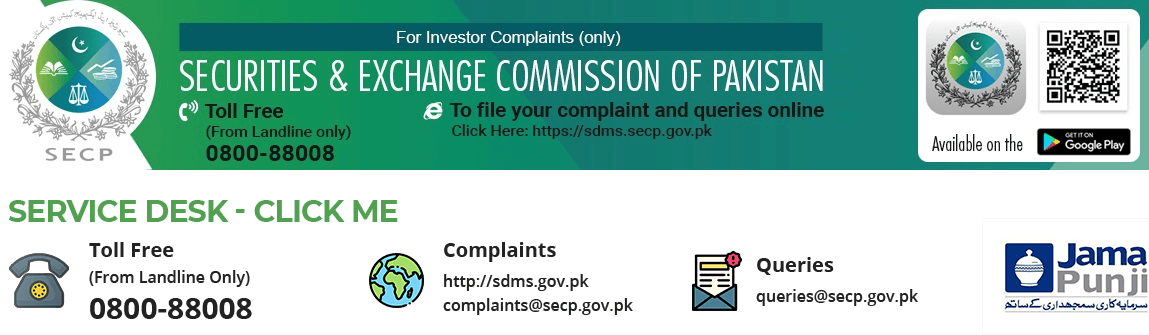

COMPANY’S OWN COMPLAINT HANDLING INFORMATION

DISCLAIMER: “In case your complaint has not been properly redressed by us, you may lodge your complaint with Securities and Exchange Commission of Pakistan (the “SECP”). However, please note that SECP will entertain only those complaints which were at first directly requested to be redressed by the Company and the company has failed to redress the same. Further, the complaints that are not relevant to SECP’s regulatory domain/competence shall not be entertained.”

Akhuwat (Registration Number 3048949, NTN 3048949) is a non-profit organization which was registered in 2003 under Pakistan’s Societies Registration Act XXI of 1860. Akhuwat is an approved NGO by Pakistan’s Federal Board of Revenue. For documentation review please click here